Amazon Q3 earnings updates: Analysts expect answers on AI progress and AWS as AMZN lags other Mag 7 stocks

Noah Berger/Noah Berger

Amazon is heading into its latest earnings report as the laggard of the Magnificent Seven this year, and investors are looking for some key updates that could spark new momentum.

Specifically, Wall Street wants to know more about its AI ambitions and how it plans to position itself against stiff competition from other Big Tech players like Microsoft and Alphabet. AWS, retail margins, and any lingering concerns over the impact of tariffs will also be on investors’ radar.

The call with analysts is scheduled for 5 p.m. ET.

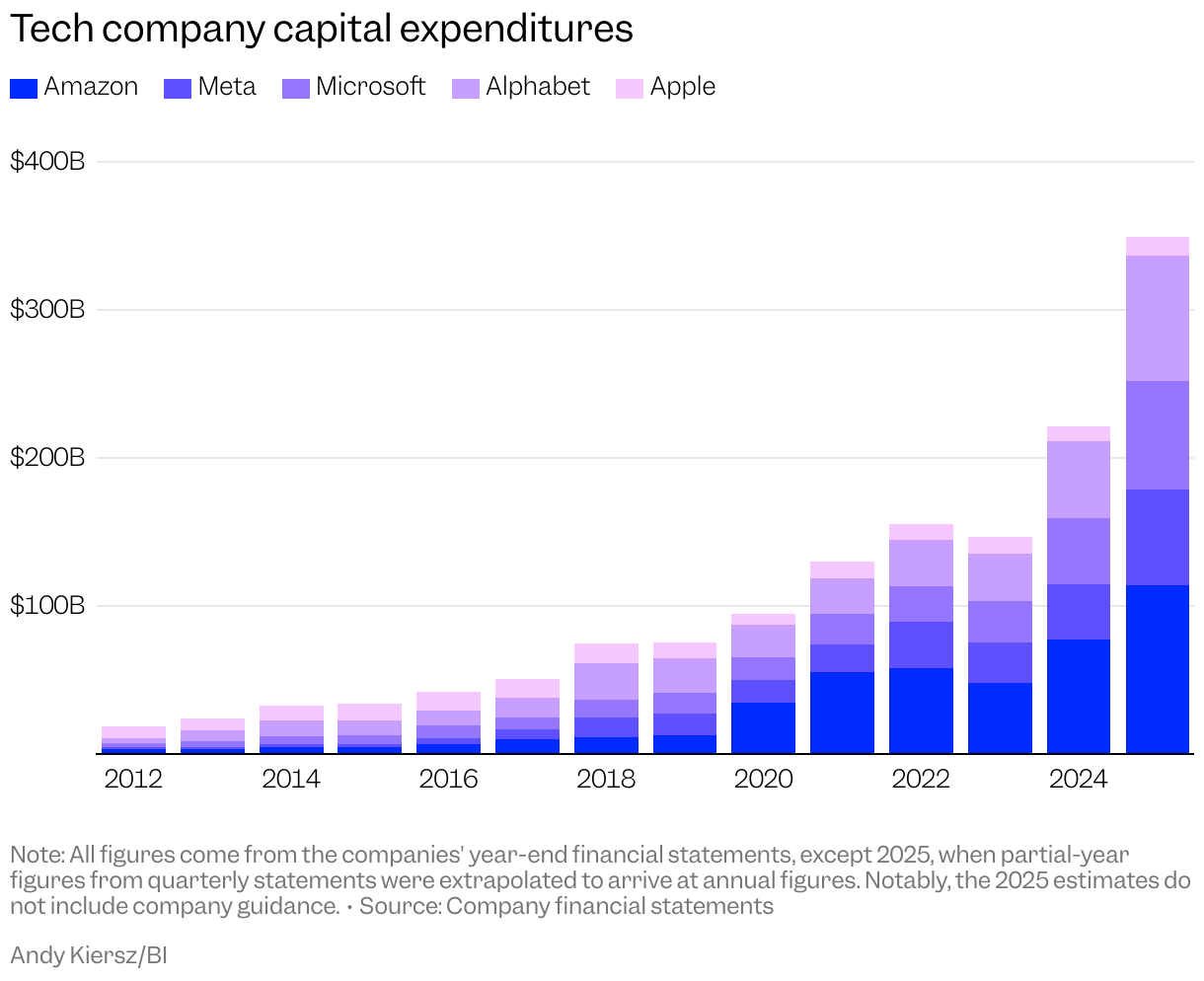

Amazon is expected to give a capital expenditures update on its earnings call this afternoon. Last quarter, Amazon’s capex totaled $31.4 billion, and the company said the figure was “reasonably representative” of its quarterly capex rate for the rest of the year. It’s largely driven by investments in AWS — particularly AI and tech infrastructure — and Amazon’s fulfillment and transportation network.

Capex growth is a hot-button issue across Big Tech. The following chart shows how spending stacks up so far.

Joe Ciolli/Business Insider