Apple earnings updates: Wall Street is bullish on iPhone demand, AI, as market cap tops $4 trillion

Written by admin on . Posted in Uncategorized. No Comments on Apple earnings updates: Wall Street is bullish on iPhone demand, AI, as market cap tops $4 trillion

Justin Sullivan/Getty Images

Hot off its historic jump to a $4 trillion market cap, Apple will report earnings for its fiscal fourth quarter after the closing bell on Thursday.

Wall Street is highly bullish on iPhone demand, which analysts see as the key driver of a consensus-beating report. Investors should also be listening for updates on the company’s AI ambitions, as some commentators this year have feared that Apple’s mega-cap peers are pulling ahead in the AI race.

The iPhone maker will report results shortly after the closing bell, typically around 4:30 p.m. ET, with the analyst call scheduled for 5 p.m. ET.

While Tim Cook has managed to curry favor with President Donald Trump, Apple has still felt the bite of tariffs — $800 million in added costs in its fiscal third quarter, to be precise.

That number was expected to grow considerably in this most recent quarter, with Apple guiding that its tariff-related costs would be around $1.1 billion.

We’ll soon see if it managed to mitigate those costs down below that estimate — or whether the impact was worse than anticipated. Analysts will also be eyeing Apple’s tariff guidance for next quarter.

With Meta’s Ray-Ban AI glasses selling well, Apple is rumored to be exploring its own smart glasses while it continues work to slim down its bulky Vision Pro headset.

When asked about the Vision Pro on Apple’s last earnings call, Cook signaled there was more to come.

“We continue to be very focused on it,” Cook previously said. “I don’t want to get into the road map on it, but this is an area that we really believe in.”

Apple is also reportedly working on some AI home devices, including one with a robot arm, as well as a foldable iPhone expected to launch as soon as 2026. Samsung, Google, and Huawei have already entered the foldable phone space.

Demand for the iPhone 17 lineup appears strong, according to third-party data, with the entry-level 17 and high-end Pro models the early standouts.

Apple’s newest iPhone lineup is outperforming last year’s models in both the US and China, two of its most important markets, according to data from Counterpoint Research. Sales of the iPhone 17 series were estimated to be 14% higher than those of the iPhone 16 lineup during the first 10 days on the market.

In the US, Counterpoint estimates that demand was strongest for the iPhone 17 Pro Max, the priciest model in the lineup, through the first two weekends of its release.

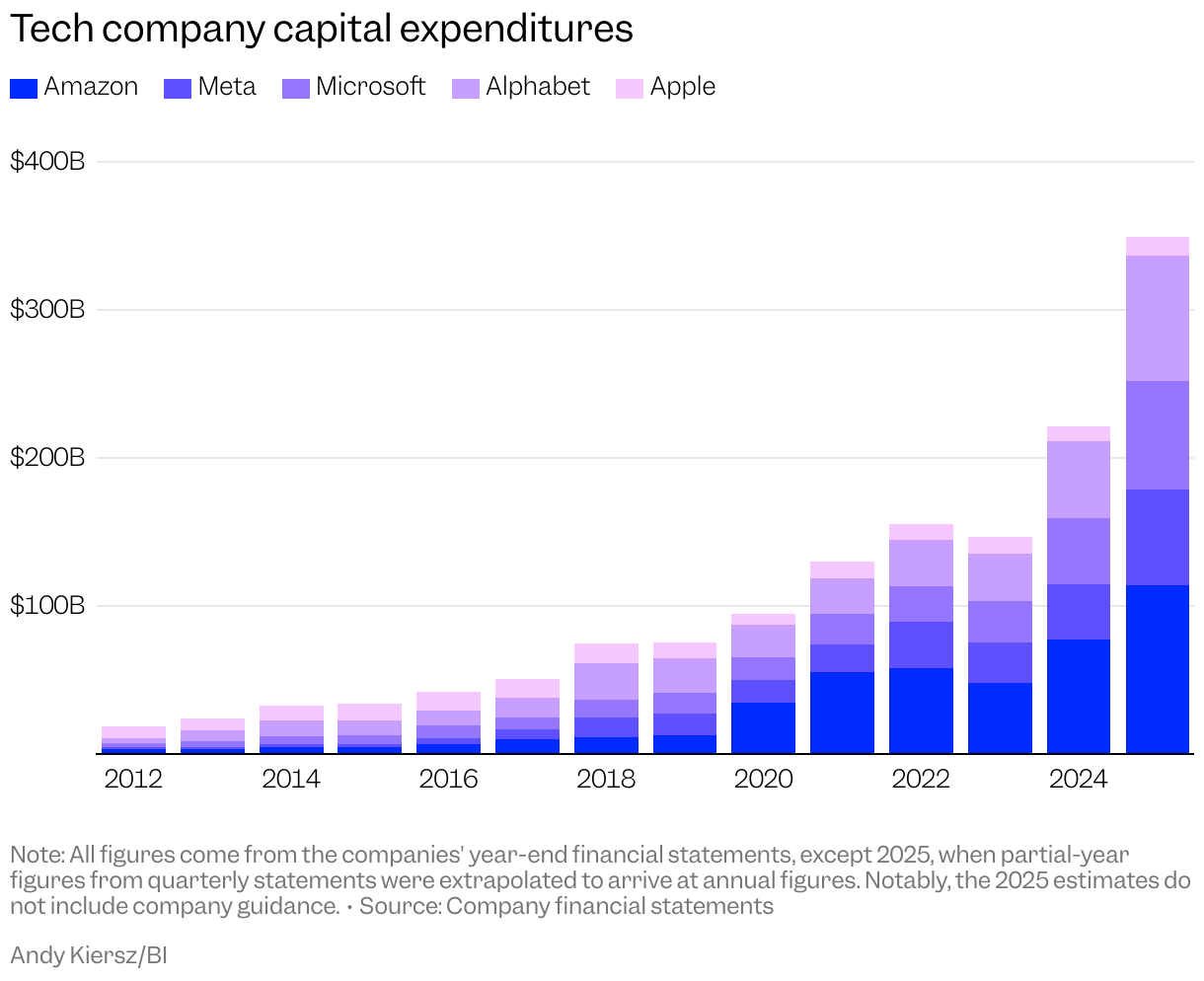

Don’t be surprised if analysts focus some questions around Apple’s capital expenditures and AI investments — it’s been a theme on other Big Tech earnings calls this week.

Tech companies are pouring more money than ever into AI, which has some investors worried. After all, the hot debate right now in Silicon Valley is whether we’re in an AI bubble…

Asked about capex growth on Apple’s last earnings call, CFO Kevin Parekh said that “a significant portion of the driver of growth that you’re seeing now is really driven by some of our AI-related investments.”

The thin and sleek form factor of the iPhone Air turned heads when it was introduced at Apple’s September event.

At 5.6 millimeters — Apple’s thinnest iPhone yet — the frame comes with a smaller battery than Pro models and no physical SIM card. To make up for what it lacks in battery life, Apple released an external battery pack alongside the iPhone Air, which costs $99. But Apple’s battery-rich Pro models, with top-of-the-line cameras, are typically the company’s most popular, and reports have begun to emerge that Apple is cutting back on Air production.

A Keybanc survey of more than 2,000 iPhone owners found weak demand for the Air model compared to the strength of the Pro and Pro Max. Three percent of respondents said they upgraded to the iPhone Air, while 41% went for the iPhone 17 Pro Max.

While Apple’s most recent quarter will only include a week or so of sales from the 17 lineup, execs will likely provide some color on how the Air is doing so far.

US shoppers discovered earlier this month that the M5 Vision Pro, a refreshed model, is labeled as being a product of Vietnam. A few creators noted the change online as they unboxed their new Vision Pros. It’s the latest example of Apple making changes to its supply chain for US-bound products to mitigate its tariff costs.

The original Vision Pro, with an M2 chip, was manufactured in China ahead of its 2024 release. Around the same time, Apple was exploring ramping up supply chain options outside of China.

Earlier this year, Tim Cook said Apple expects “the majority of iPhones sold in the US will have India as their country of origin” in the June quarter.

Don’t be surprised if Tim Cook leans into Apple’s work in the US.

Earlier this year, Cook committed to investing $600 billion in US manufacturing amid President Donald Trump’s tariff push. In August, Cook presented Trump with a gift, an American-made glass plaque set on a 24-karat gold base.

Cook has proven to be a savvy political navigator — and it appears to be paying off. After receiving the gift, Trump said companies like Apple “will be treated really well.”

Cook, alongside other tech leaders, joined Trump for a dinner event in September. The Apple CEO addressed the president in a speech, praising his efforts to bring more manufacturing to the US.

Earlier this week, Nvidia CEO Jensen Huang gave an America-themed presentation during Nvidia’s GTC October keynote.

There’s an argument to be made that Apple’s slow start in AI hasn’t hurt it all that much — at least not yet. Yet with all the headlines around its AI talent departing, Apple would do well to reassure the market that big and exciting things are coming. One of those is a long-anticipated overhaul of Siri with Apple Intelligence, touted for next year.

Then there are reports of new home devices and AR glasses — all of which will need good AI. Don’t expect Tim Cook to break character and start gossiping about future products, but this would be a good time for a bit of extra candor.

Apple looks like it’s in a better position heading into its earnings report than it has been in a year, according to Angelo Zino, a senior equity analyst at CFRA Research.

Zino pointed to how investors now have more clarity relating to Apple’s regulatory issues and the potential impact of tariffs.

“Recent comments about tariffs tied to the company from the Trump administration make us feel much more comfortable about the margin outlook ahead,” he added.

Demand for iPhones also looks solid heading into the print. CFRA said it was “conservatively” estimating that iPhone revenue was on track to grow 6% for the current quarter and 5% for the upcoming quarter.

CFRA issued a “Buy” rating on Apple and a $280 price target, implying 4% upside from the stock’s current levels.

Bank of America has a strong outlook for Apple over the next five years. Analysts pointed to revenues potentially increasing due to AI and its possible impact on coming product offerings.

Analysts also said they saw “strength” in new iPhone demand, and estimated that total iPhone unit sales could reach 57 million for the current quarter, compared to consensus estimates of 54 million.

“Reiterate Buy on strong capital returns, eventual winner in AI at the edge & optionality from new products/markets,” BofA said on their rating of the stock.

Analysts lifted their price target for the stock from $270 to $320 a share, implying 19% upside from Wednesday’s price.

JPMorgan said it expected Apple earnings to “track modestly better” from September through the end of the year, thanks to strong demand for the iPhone 17.

The bank also said it expects Apple to post solid revenue growth in the first quarter of its 2026 fiscal year.

“AAPL shares are heading into the upcoming earnings print with a greater halo of positivity than any time in the past year,” analysts wrote in a recent client note, adding that they believed that chatter around Apple’s investment thesis had narrowed down to the strength of new iPhone sales.

Apple stock could be boosted by a few catalysts contained in its report, Melius Research said.

The research firm said it believed that the company’s sales in China would pick up over the near term. Profit margins could also improve on demand for Apple’s new lineup of iPhones, analysts said, adding that they believed Apple was “getting its groove back.”

“We think there is more to go as a beat and raise could be on the horizon when it reports,” analysts wrote of the stock’s momentum.”Bottom Line: Apple is on a mission to silence its critics. We see upside to sales in China into CY26 and momentum in new models overall.”

The firm reiterated its “Buy” rating on the stock and issued a price target of $290 a share, implying 8% upside from current levels.

Analysts at Goldman said they expect Apple to beat on earnings for the quarter, driven largely by strong demand for its new iPhones.

The bank estimated that iPhone product revenue could see a 10% year-over-year increase to $50.8 billion, compared to the consensus estimate of $49.8 billion in revenue for the quarter.

Apple could also see its services revenue grow 13% year-over-year, thanks to continued momentum across subscription services like iCloud+ and AppleCare+, analysts added.

Still, “key areas of debate” among investors include the sustainability of iPhone demand due to trade policy uncertainty, as well as risks to the company’s App Store revenue, the bank said.

Goldman reiterated its “Buy” rating for the stock and issued a price target of $279 a share, implying 3% upside from current levels.

Fourth Quarter

- Revenue estimate $102.19 billion

- Products revenue estimate $73.49 billion

- Mac revenue estimate $8.55 billion

- iPad revenue estimate $6.97 billion

- Wearables, home and accessories estimate $8.64 billion

- Services revenue estimate $28.18 billion

- Greater China rev. estimate $16.43 billion

- Americas rev. estimate $44.45 billion

- Europe revenue estimate $26.36 billion

- Japan revenue estimate $6.41 billion

- Rest of Asia Pacific revenue estimate $8.08 billion

- EPS estimate $1.77

- Total operating expenses estimate $15.75 billion

- Research and development operating expenses estimate $8.8

billion - SG&A operating expense estimate $6.96 billion

- Gross margin estimate $47.41 billion

- Cash and cash equivalents estimate $51.67 billion

- Cost of sales estimate $54.47 billion

- Total current assets estimate $144.92 billion

- Total current liabilities estimate $159.68 billion

First Quarter

- Capital expenditure estimate $3.97 billion

2026

- Capital expenditure estimate $15.03 billion

Source: Bloomberg